Get Health Insurance

After a Qualifying Life Event

Enroll outside Open Enrollment: Get A Quote In Minutes:

No spam. No obligation. Just real support. One licensed agent will reach out to review your options.

Trusted by families nationwide looking for affordable alternatives to COBRA and marketplace plans:

Greg T - Greg T.

Greg T

Adrienne and Chris are super helpful and will go out of their way to make sure whatever I need is done. - Austin P.

Adrienne and Chris are super helpful and will go out of their way to make sure whatever I need is done.

If you have recently lost coverage, changed jobs, gotten married, had a baby, or moved, you may qualify for a Special Enrollment Period even if Open Enrollment is closed.

Americans deserve affordable healthcare. And you do not have to wait to get it.

Many families are shocked to learn that COBRA premiums can exceed $1,500 per month and ACA plans often come with $9,000 or higher deductibles before benefits really kick in.

Families in these situations can often avoid COBRA and overpriced marketplace plans by shopping for a private PPO option that offers no out-patient deductible, $0 copays, and coverage that travels with them nationwide.

What Is A Qualifying Life Event?

It's a major life change that allows you to enroll in health insurance outside the yearly Open Enrollment period.

If one of the events below happened recently, you may be eligible to enroll right now and avoid going uninsured or overpaying for COBRA.

This includes between jobs, reduced work hours, COBRA ending or becoming too expensive, or really any loss of employer coverage.

Getting married, divorced, or legally separated can open a Special Enrollment Period so you can update or replace your health coverage.

Having a baby, adopting a child, or welcoming a foster child allows families to enroll or adjust coverage outside Open Enrollment.

Moving to a new state, county, or ZIP code that offers different health plan options can trigger Special Enrollment.

Certain income changes, changes in citizenship or immigration status, or other qualifying circumstances may also open enrollment. A licensed agent can confirm eligibility.

Not sure if your situation qualifies? Most people aren't and that's exactly what we help with.

Why families choose American Ally:

Smart Benefits

With Year-Round Support

Our health insurance premiums are typically 40%-50% lower than ACA plans or COBRA for qualifying individuals or families and come with incredible benefits:

Leave your cash at home!

You can enjoy $0 copays when visiting the doctor, specialist, urgent care, and MORE.

Start using benefits like dr visits or urgent care day 1 - with NO deductible.

The only time a deductible applies is if you're in the hospital for more than 24 hours—and even then, you choose the deductible that fits your budget upfront so there are no surprises later.

With access to one of the largest PPO networks in the country our members have no trouble finding doctors - in fact, your doctor is probably already in-network!

Simply show your card and see your doctor - no copay, no hassle.

Real people. Real help.

You’re never alone here.

Our Patient Advocates are experts in medical billing and insurance. From finding doctors to pre-pricing procedures to filing claims and even negotiating surprise bills—they’re just a phone call away.

Flexible plans that put you in control.

Whether you're covering a family, spouse, child, employee, or just yourself, you'll have the flexibility to build a plan around your needs and budget!

Real People. Real Protection.

When David* was diagnosed with cancer, he braced for the worst—not just medically, but financially. The treatments came quickly, and so did the bills.

But with the help of his private PPO plan, what followed wasn’t panic: it was relief:

He was able to get the treatment he needed, when he needed it.

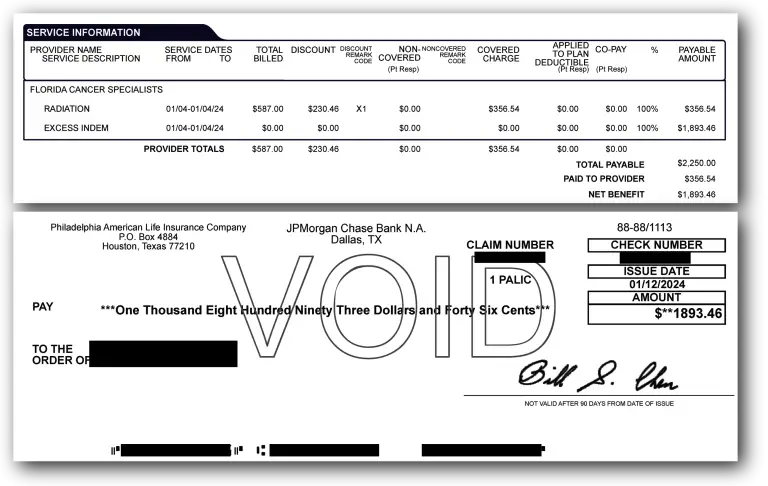

Florida Cancer Specialists billed David's plan $356.54 for his treatment. (pictured)

David's plan has $2,250 of coverage for radiation treatment, so his plan paid Florida Cancer Specialists their $356.54 and sent David a check for the remaining $1,893.46 (pictured)

David will get a check like that every day he goes in for treatment, up to his calendar year max, and he is free to spend those checks however he needs too.

I spoke with a licensed agent who showed me how I could stay on my employer plan for about $19/month—and move my husband and kids to a more affordable private PPO plan.

That one change saved us over $652/month—more than $7,000 a year back in our pocket."

(*Name and identifying details changed for privacy.)

How Special Enrollment Works

Most Qualifying Life Events provide up to 60 days from the date of the event to enroll. Missing this window may leave you stuck with COBRA (COBRA is optional) or uninsured until Open Enrollment in November.

Follow these 3 easy steps to request a quote and see if you qualify:

We Handle the System,

So You Can Focus on Healing

You get year-round support from U.S.-based Patient Advocates, who are experts in medical billing and make your care Significantly simpler and more affordable.

Patient Advocacy is a voluntary membership and not an insurance product.

Our advocacy team can shop the cost of your health care for you and present fairly-priced options within your benefits.

Never worry about surprise bills again! Our experts can review your bill and negotiate with providers on your behalf.

Our advocacy team handles the claims process for you, so you can get reimbursed sooner.

Just let our team know what kind of doctor you need and they'll do the digging for you to find primary care, specialists, facilities, and more!

Top Questions About

This Private Health Insurance Plan

Can I get health insurance outside Open Enrollment?

Yes. A Qualifying Life Event may allow you to enroll during a Special Enrollment Period.

How long do I have to enroll after a Qualifying Life Event?

In most cases, up to 60 days from the date of the event. Timing matters.

Do I have to choose COBRA if I lose my job?

No. COBRA is optional. Many people qualify for more affordable alternatives during Special Enrollment.

Is This Real Health Insurance?

Yes! This is a health indemnity plan that is approved and regulated by each state’s Department of Insurance.

Is This a PPO, HMO, or EPO plan?

This is a PPO plan, giving you access to one of the largest provider networks in the country - nearly 96% of the U.S. population has a provider within 20 miles.

Is My Doctor In-Network?

Because this plan gives you access to one of the largest nationwide PPO networks, it is very likely that your doctor is in-network. Your agent can verify that your doctor is in-network before you apply!

Is There A Max Out Of Pocket?

Our plans don’t have a traditional out-of-pocket maximum. Instead, you select your annual benefit limit, choosing from $250,000, $500,000, or $1,000,000 in coverage for the year. This allows you to customize your plan to match your healthcare needs and budget.

Do I Qualify?

Most healthy Americans do qualify, however this plan may not be the right fit if you have any of the following:

- Recent heart attack or stroke

- Current cancer or a history of cancer within the last five years

- Insulin-dependent diabetes

- Pregnant

- COPD

- Need for immediate surgery

- Age 65 or older

If none of these apply to you, then you'll probably qualify, and don't worry, conditions like high blood pressure, high cholesterol, or other minor health issues won’t prevent you from qualifying either.

If You've Experienced A Qualifying Life Event, Your health insurance options may have changed.

Compare your options and avoid expensive COBRA plans:

Greg T - Greg T.

Greg T

Adrienne and Chris are super helpful and will go out of their way to make sure whatever I need is done. - Austin P.

Adrienne and Chris are super helpful and will go out of their way to make sure whatever I need is done.